Every dental migration route holds dozens of foreign-currency payments — from the ADC's AUD 647 assessment to thousands in exam fees and tuition — and all of them hit the same wall: the international payment system is closed to Iran. This article, with no promise of shortcuts, lays out the real options with their risks, so your payments both arrive and never come back to haunt you.

A plain disclaimer first: this is information, not financial or legal advice; sanctions rules change, and responsibility for every transaction rests with the payer.

Why the normal rails are closed

The global payment services — Wise, PayPal, Remitly, and their peers — do not serve Iran under sanctions, and Iranian bank cards are not accepted by foreign payment gateways. So every payment you make travels one of three roads: your own foreign account, the account of a trusted intermediary, or an exchange/remittance service.

Option one: a bank account outside Iran — best, where possible

If you, your spouse, or an immediate relative holds a solid account in Türkiye, the UAE, Armenia, Georgia, or the destination country, the cleanest pattern is: fund that account through a reliable channel, and make every official payment from that single account. The advantages: a uniform payment history, an international card for time-critical registrations (remember how ADC practical seats vanish within hours?), and simple source-of-funds proof. Many candidates tie opening that account to one of their exam trips (Istanbul, Yerevan, Dubai); requirements for Iranian citizens vary by country and bank and have tightened — check the bank's current rules before travelling.

Option two: the diaspora's exchange and remittance services

For payments without a personal account, licensed exchanges and the services established in the migrant community are the standard road — names like IranianCard, Kangaroo Exchange, MoneyMex, Rose Cap, Alaeddin, and 20Payment recur among users across destinations. Naming them is a statement of existence, not an endorsement; before any large transaction: verify licensing and track record, test with a small amount, compare rates and fees across two or three services, and collect a complete receipt.

The risk that grew in 2026: secondary sanctions

Since February 2025 the US Treasury (OFAC) has designated more than a thousand Iran-linked persons, companies, and vessels in its new campaign, and in January 2026 six Iranian crypto exchanges were specifically designated. The practical meaning: using a designated channel — even unknowingly — can create secondary-sanctions exposure for sender, receiver, and the banks in between; and your destination account (the one you just opened in your new country) is exactly where that risk surfaces: freezes, questioning, or closure. The simple rule: remove crypto and anonymous channels from your migration payments, and stay loyal to transparent, documentable rails.

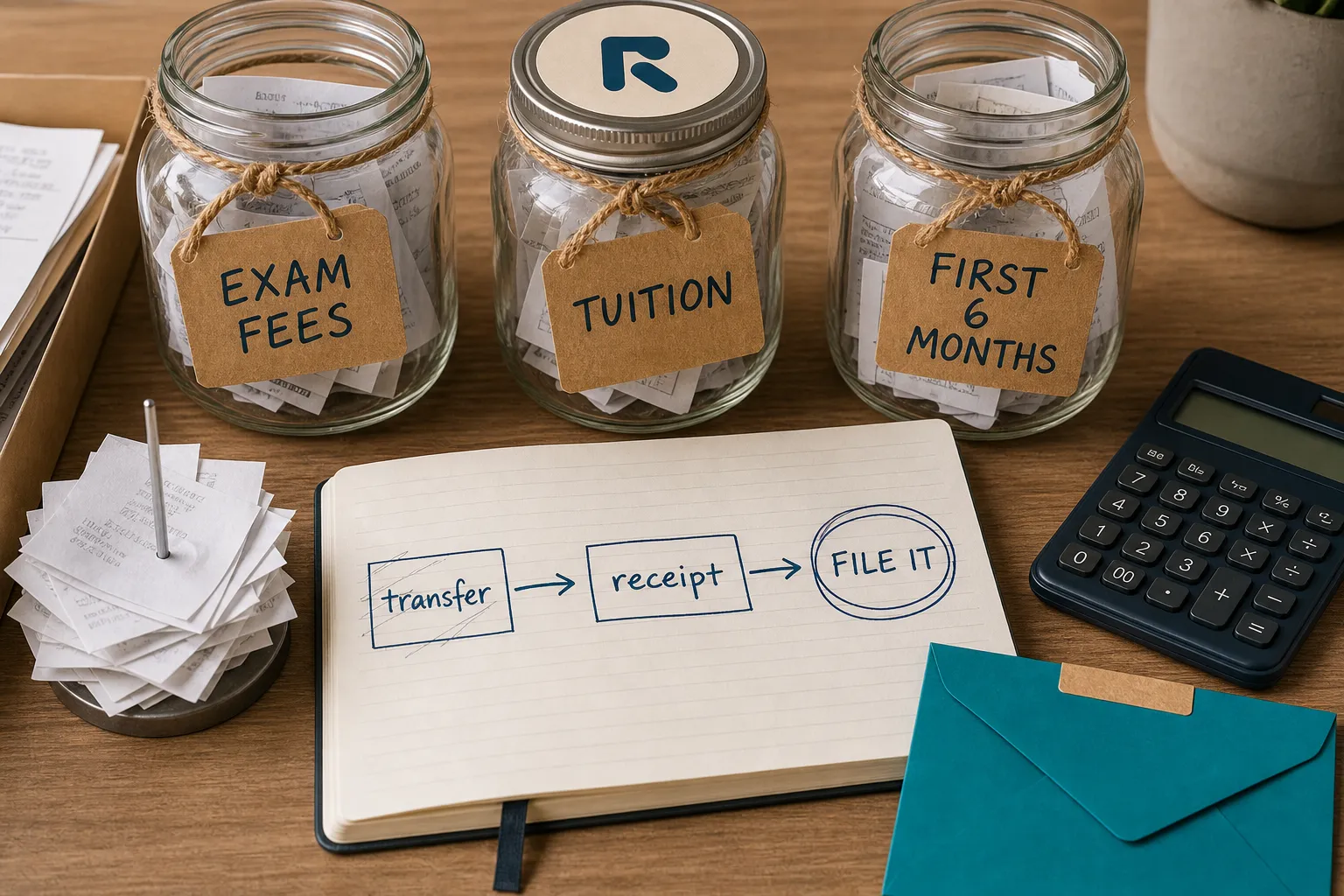

Documentation: the folder that saves you later

Destination banks are sensitive about Iran-linked inflows — not necessarily hostile, but inquisitive. For every payment and every account top-up, archive four things: the transfer receipt with the service's details; the source-of-funds document in Iran (a property sale, savings, practice income — official records or bank statements); the exchange rate and date; and the payment's link to your migration (the exam or tuition invoice). The day a bank officer in Toronto or Melbourne asks about a forty-thousand-dollar deposit, that folder is the difference between a five-minute chat and a frozen account.

Managing rial volatility: the three-part rule

The rial has covered breathtaking ground in two years — from about 817,000 per dollar in January 2025 to a record 1.42 million in December 2025, then high-band volatility through 2026 (with the remittance rate typically above cash). Three working rules: First, convert near-term committed costs (a booked exam, next term's tuition) early; the risk of a rate jump outweighs the possible gain from waiting. Second, never convert the whole budget at once; stage it across several tranches. Third, date-stamp every local-currency estimate in your plan and re-price it on payment day — a six-month-old estimate is not a document.

Three special payments, one note each

Government fees (visas, IRCC, the Home Office): only through the official channel that body names; "we'll register for you" intermediaries add file-error risk. Large tuition (QP/IDP): before transferring, write to the university's finance office about accepted routes for students from sanctioned countries; most have experience and a path. Exam-trip money: keep travel funds separate from the payments budget; mixing the two muddles both the accounting and the documentation.

Frequently asked questions

How do I handle registrations where seats vanish in hours? Have an active, tested international card — yours or a trusted person's — ready in advance; registration moment is no time to trial a new channel. Park the amount on that card beforehand.

What will the destination bank ask me? Three standard questions: source of funds, the transfer route, and your relationship to the sender. The right answer is that documentation folder: the sale/savings record plus the exchange receipt plus a short written explanation. The wrong answer is "I don't know, a relative sent it."

Move the money at once, or in instalments? For visa proof-of-funds, money settled and documented early beats a sudden deposit; for running costs, staged transfers spread both rate and channel risk. The standard blend: settle the core budget early, then smaller periodic transfers.

Will a third-country account (Türkiye/Armenia/UAE) cause trouble later? The account itself, no; what raises questions later is undocumented transactions. The same rule as ever: every inflow and outflow gets a receipt and a written reason.

When should I buy currency? We offer no speculation — only risk management: lock the near, certain costs early, stage the rest, and never chain a big decision to a rate forecast. The 817,000-to-1.42-million swing of these two years is the whole argument.

The final toolkit: five documents to keep current

One: a table of upcoming costs with currency and due date. Two: the transfer-receipt folder (PDFs, date-stamped names). Three: source-of-funds records (sales, savings, income) with certified translations. Four: your tested channels list with each one's fee and timing. Five: a note of every transaction's exchange rate. Those five serve the destination bank, the visa file (proof of funds), and your own peace of mind — and collecting them from day one is far easier than reconstructing them on the day of need.

The payment problem is solvable — thousands of your colleagues have solved it — on three conditions: transparent channels, obsessive documentation, and respect for secondary-sanctions risk. Hold those three and money will never be your bottleneck; the full route budgets live in the five-country cost comparison.

Each destination's exact costs: Australia • Canada • UK • Germany